Central Banks, Global Debt & COVID

by Robert W Malone MD, MS | Jul 26, 2022

I first met Ed Dowd during an early trip which a group of physicians from the International Alliance of Physicians and Medical Scientists (www.globalcovidsummit.com) made to the Hawaiian Islands of Maui and Oahu during the fall of 2021. The primary purpose of the trip was to support our physician colleagues Dr. Kirk Milhoan (MD, PhD- Pediatric Cardiologist) and Lorrin Pang (MD, MPH- Maui County Public Health Officer), who were embroiled in an effort by local press and politicians to take their medical licenses for the perceived infraction of supporting early COVID treatment and (in the case of Lorrin) relying on his own evaluation and interpretation of the safety and effectiveness of the COVID-19 genetic vaccines. The particular grievance concerning Lorrin seemed to have revolved around his reservations concerning the lack of data demonstrating safety of SARS-CoV-2 genetic vaccination during pregnancy. After many long months subjected to the usual defamation and derision in local corporate-controlled media, both were eventually exonerated. No final action was taken against them by the Hawaiian medical board, although both were deeply impacted by the experience, and I suspect will forever be more guarded and defensive in their medical practices.

It was during a local group dinner and fundraiser for the cause, held on the island of Maui, that Ed and his colleagues first introduced themselves to me. To my surprise, they indicated that they had authored a document which they named “The Malone Doctrine”. Taken aback, as neither Jill nor I had contributed in any way, I asked why they were using this name. Ed and his colleagues told me that “we have read and listened to everything you have said and written during COVID, and this is what is written in the white spaces between every line”. The wisdom and clarity which they captured in that document has become a guiding light for many since it was published, and their “Malone Doctrine” provides the basis for every statement regarding integrity which I have made since that time. But where did this profoundly prescient document come from? A dedicated team which included a senior building inspector (buildings need integrity also!), some young hardworking idealists, and an experienced hedge fund manager- Ed Dowd. Their “Malone Doctrine” was written to address what they saw as a fundamental societal breakdown in commitment to integrity. Not just for the US Department of Health and Human Services, but for virtually every “vertical” sector throughout society, government and particularly large businesses. We hear a lot about ESG (environmental, social, and governance) scoring from big business and the investment firms that control the large firms, but not much about integrity.

Only a few financial industry “insiders” had heard of Ed Dowd at that point, but as Jill and I came to know him better over the ensuing months, we realized how special both Ed and his team of integrity advocates actually were. And then, one day, Ed brought to my attention the emerging data concerning all-cause mortality being revealed by senior life insurance executives. He thought that this was big. These data seemed to cut through the obfuscation, the fog of government and corporate media misrepresentations and propaganda concerning the vaccine – associated adverse events. These were data coming from a completely separate source relative to the various government-controlled “safety” databases, and what these new data revealed raised profound questions about the official narrative of safe and effective genetic vaccines. I did my best to help introduce Ed to the world and connected him to various leaders in the alternative independent media, and the rest is history. Ed Dowd is now widely recognized for his insights, integrity, clarity of thought, and courage.

I asked him to write a chapter and tell the story of his journey for this book, and am grateful that he was able to find the time. There have been so many heroes who have stepped up to meet the challenge of the COVIDcrisis, and Ed and his Hawaiian colleagues are certainly on the short list of the bold and brave. I hope you enjoy and learn from this account of what he has experienced and observed during these trying times.

Central Banks, Global Debt & COVID

My journey into the world of fraud began long before the Covid 19 Vaccine fraud. I have spent the majority of my career on Wall Street at firms like HSBC Inc., Donaldson Lufkin & Jenrette and BlackRock. I learned about fixed income, currency, & equity markets through my time at these institutions. My knowledge of global capital markets is very deep.

The Enabled Central Bank DotCom Fraud

My first introduction to fraud began on Wall Street after I received my MBA from Indiana University, I was a young electric utility analyst in the research department of Donaldson Lufkin & Jenrette from 1997 to 1999. The firm was sold to Credit Suisse Bank years after I left but the firm was known as a premier stock research firm and was referred to as “The Investment House that Research Built.”

In my time there I witnessed the internet teams in research grow large, as they were in the middle of the DotCom boom and were busy bringing to market IPOs of internet companies that were sprouting up by the hundreds if not thousands. It was a heady time, and companies with not much in the way of revenues were quickly run through the due diligence process and deemed acceptable for investors. The demand for these IPOs seemed insatiable, and the money pouring into the bank from the fees was eye popping. Needless to say, the party continued, and the deals became more ridiculous, but the stocks of these future worthless companies continued to rise as demand for what was called the ‘New paradigm” continued apace. The belief then was that the stock market is forward looking, and these companies would disintermediate all the boring old brick and mortar companies that had real capital investments and take over the world. As a backdrop though, and what people couldn’t see at the time, was that the Federal Reserve was providing (by historical standards then) very accommodative monetary policy as the world was deathly frightened by the Y2K phenomenon. The easy money found its way into this speculative craze, and I witnessed my first mass formation psychosis event amongst the professional investment crowd. This easy money also found its way into junk bonds, which also provided another source of capital for these newly created companies. Flush with IPO cash and junk bonds, these revenue challenged companies went on a buying binge of epic proportions and bought real estate, software products, and hired countless people. The end result of all of this was creation of an explosion of growth in Nasdaq tech companies’ top line as they provided the arms to these new companies to take over the world. The Nasdaq bubble was born, and the party lasted until the Federal Reserve began raising interest rates and took away the easy accommodation. The first companies to implode were those with no revenues, and their funding dried up. The cascading effects lasted 2 years, and the US economy went into recession. As always, easy money leads to fraud and the corporate accounting frauds of Enron, World Com, Lucent, Nortel & Quest all came to light. These real firms all fed off the easy money created by the new companies’ capital spend and the trend of hype. Many of the newly created companies engaged in revenue fraud as well, where they had back door agreements to purchase items from each other to create the illusion of growth. It was a halcyon time for fraud and malfeasance.

The key thing to remember is that the easy money from the Federal Reserve was responsible for speculation, which in turn led to a gigantic misappropriation of capital that ended up driving tremendous losses, fraudulent behavior and theft. Without easy money none of this would have happened.

The Cycle Begins Anew: Central Bank Enabled Housing Fraud

A recession began in 2000, and the Federal Reserve began the cycle anew by lowering interest rates to temper the popping of the Nasdaq bubble. In 2002, I became a portfolio manager for BlackRock, and began managing a large cap growth equity portfolio. Over the next 5 years we navigated our fund through the next Fed bubble that was blowing. That bubble was real estate. It began innocently enough, but quickly moved to speculation which led to excess and fraud. The difference with this bubble (unlike the last bubble which was the consequence of corporate fraud), was that this fraud found its ways onto the balance sheets of banks, investment banks & insurance companies. Wall Street began to develop ways of slicing and dicing the risk of single home mortgages into exotic bonds called Collateral Debt Obligations (also known as CDOs). It began innocently enough, but over time loans were made to people who had no ability to own a home, and the fraud went into high gear as liar loans became an industry standard. The rating agencies which gave triple AAA ratings to the supposedly safest tranches of these CDOs began to look the other way due to the practice of receiving a fee for rating the bond. The volume of CDOs being produced by Wall Street was so large that the intuitional imperative took over and greed ruled the day.

Towards the end of this cycle, the refrain from the true believers to the skeptics was that “Home Prices Never Go Down.” The Federal Reserve started raising interest rates in 2006, the party started to unwind in 2007, and then cascaded into the Great Financial Crisis of 2008-2009. The formerly rated AAA bonds imploded 60% in price, and if the Federal Reserve had not begun the unprecedented action of bailing out banks and insurance companies by buying these fraudulent bonds (which remain on the balance sheets of the central banks today) it is quite likely that we would have seen a collapse of the entire western financial system.

It’s important to remember that not one banker went to jail for these crimes. Thus began the rise of global central bank dominance, and this was facilitated by unprecedented cooperation between the US Federal Researve, the EU Central Bank and The Bank of Japan in the form of money printing and debt purchases. The global governments of the world went into deficit spending to make up for the catastrophic wealth destruction, job losses and demand destruction.

The Most Recent Cycle: Central Bank & Political Fraud with COVID as the Cover Up

The free markets (as we previously understood them) ended on March 5th, 2009, when the Fed began its historic bailout of the banking system. The last 12 years have seen an unprecedented growth in Global debt to keep the patient known as the Global economy on life support. Crony capitalists and those closest to the money printing machines have seen their wealth grow, while the rest of the citizenry have been lucky to march in place and not give up ground economically. Washington DC’s power and wealth have increased mightily since that crisis unfolded. The percent of GDP that the government now commands is 40% thanks to the COVID crisis and is up from low double digits 40 years ago.

Many of us in the financial community had wondered what the end of this cycle would look like? We knew that all cycles end, and that the growth in global debt which was in progress was unsustainable. How would it manifest, we pondered: Political Instability? Currency Wars? Kinetic War? Sovereign Debt Defaults? In 2019 we saw the beginnings of global growth slowing and a repo crisis, where overnight lending rates spiked in the fall. Corporate credit spreads began to wobble a bit and it looked like we were nearing the end of this cycle. Then the COVID 19 crisis hit, and the central Banks had an excuse to print the largest amount of money in the history of the federal reserve, with an increase of M1 by 65% from 2019 to 2020 (M1 money supply encompasses physical currency and coin, demand deposits, traveler’s checks, and other checkable deposits).

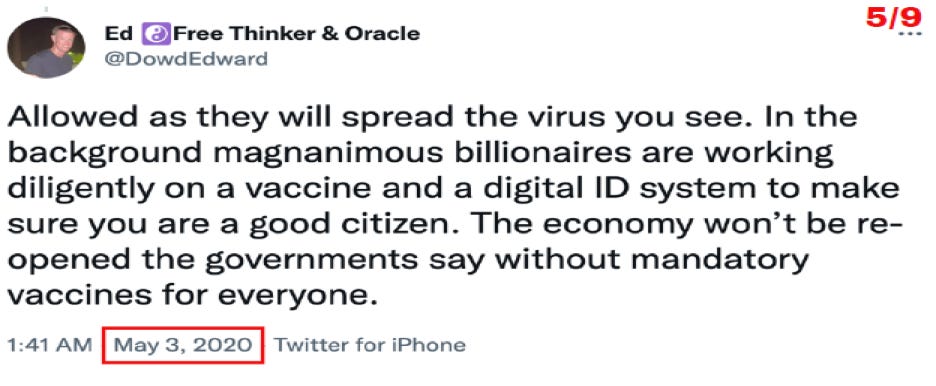

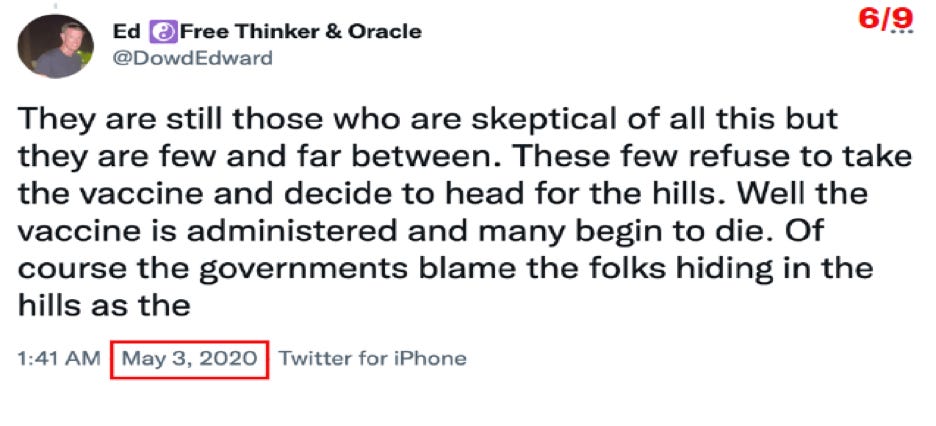

As a seasoned investment fund manager, my suspicions were triggered by this surge in M1. My suspicions were confirmed when I saw Saint Louis Federal Reserve President of James Bullard being interviewed about how to reopen the economy during the April 5, 2020 edition of the Sunday show “Face the Nation”. I began suspecting that COVID was being used as cover for a new global financial collapse. Bullard indicated that we had new technologies that could test people, and those with a negative test could wear immunity badges and with new surveillance technologies which would enable them to be tracked. I was simply blown away. Why was a Federal Reserve President weighing in on public health? I speculated that once a vaccine was introduced, governments would begin to implement vaccine passports. For raising this concern during 2020, I was labeled a conspiracy theorist. Fund managers such as myself typically operate based on various models which they develop to explain long and short term political and economic trends. On the basis of the events and public statements (from Bullard and others) which were circulating, I developed a working thesis that COVID would be used as an excuse to control travel and clamp down on global riots once the debt collapse began in earnest. The collapse of the world’s economies could easily be blamed on COVID and ensuing “safety” measures would be put in place as a system of control and compliance- for our own good. Also, continued virus evolution and outbreaks could be used as additional excuses to print more money by the central banks. Under this theory, the vaccine passport was merely a gateway device for what would eventually become a central bank digital currency system that would monitor vaccine compliance and institute a social credit score to make sure you were a good citizen.

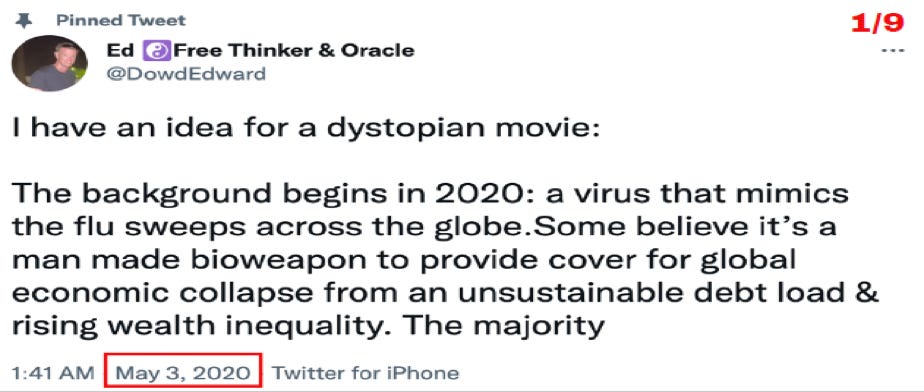

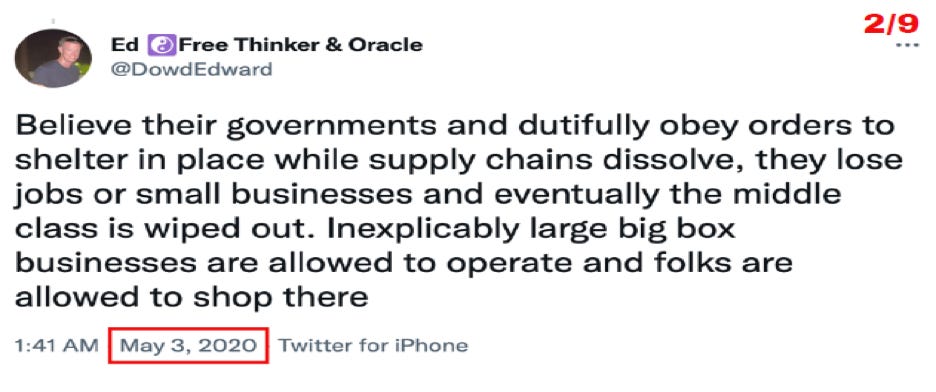

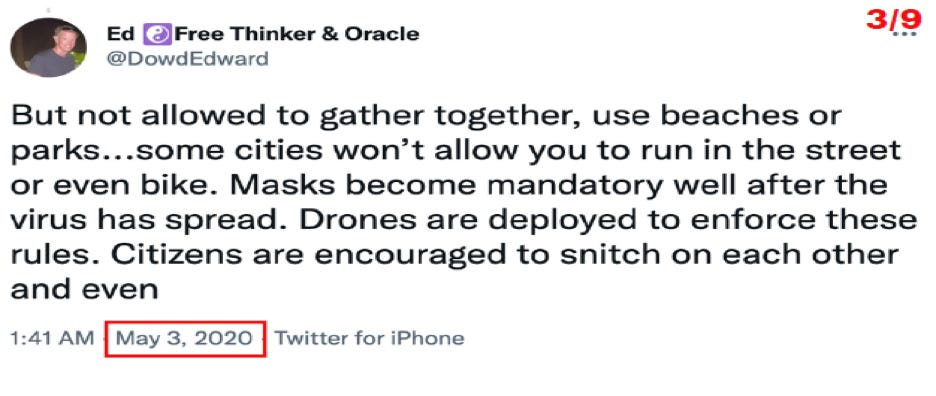

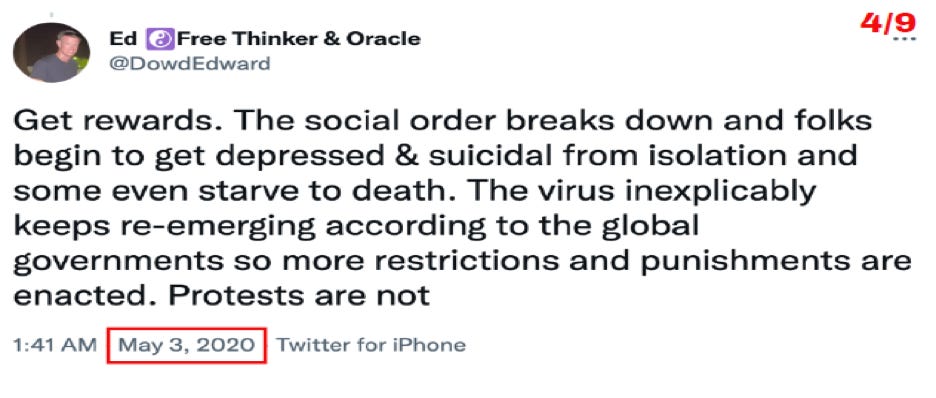

To memorialize this thesis, I developed a twitter thread beginning May 3, 2020 which predicted what might unfold over the next 2 years. However, since these ideas seemed so dystopian at the time, I couched my predictions in the form of a dystopian movie script concept. What follows are tweets from that time:

My predictions were all predicated on the thesis that COVID was cover for the end of the global debt bubble that had its origins in 1913 (when the Federal Reserve System was created). Most of what I predicted in these tweets came to pass with vaccine mandates, vaccine passports and the othering of the unvaccinated. We can all recall that the President of the United States (along with many others) blamed the unvaccinated for the continued spread of the virus at the end of 2021. Throughout all of 2021 the refrain by the establishment was that the vaccines were “Safe & Effective!” In reality, we have also learned that these injected pharmaceuticals are the deadliest vaccines ever created in the history of man, with countless deaths and injuries, all of which have been suppressed by the media and our governments. We have also discovered that the mRNA vaccines not only don’t work, but also select for the continued viral evolution which has resulted in the vaccinated disproportionally suffering ill effects of COVID relative to the unvaccinated. Finally, just as I had imagined during May 2020, we did witness draconian censorship and the smearing of any credentialed experts who deviated from the establishment narrative.

How I became Involved in the Fight for Freedom & The Malone Doctrine

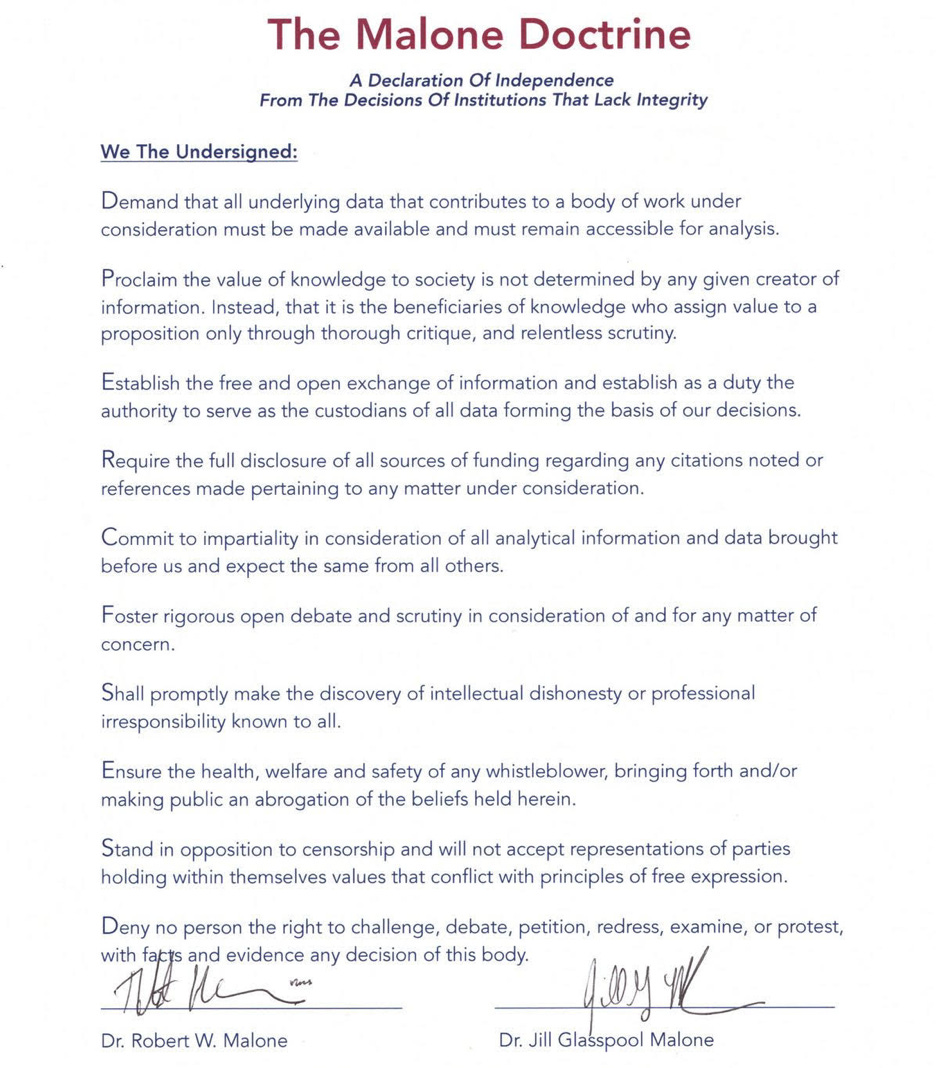

In September of 2021, I became very distraught while watching my predictions unfold before my eyes. All over the world, societies were falling into a dystopian nightmare that most of the people around seemed to be fine with, as they gave their freedoms away without so much as a single thought or suspicion. There were a number of residents on Maui who did consider the draconian mandatory vaccines and passports an assault on our freedoms. I attended the multiple local allies and protests which ensued. I met many different kinds of people that all had one thing in common…a belief in fundamental bodily sovereignty. There was no red team-blue team dynamic, but rather a wide range of different races and creeds and belief systems were represented. We began to call ourselves team humanity. It was at one of these rallies I met Tom Lewis, who informed me that Dr. Malone was coming to the island to help some local doctors fight the medical censorship that was descending within the medical community. A series of private dinners were set up, and Tom wanted me to attend. Steve Kirsch was also in attendance on the island, and he was also present at the dinners as well. Dr. Malone spoke passionately at the dinners about the corruption of our institutions. Local colleagues including Tom, myself, Barry O’Keefe and Andrew Aker attended the dinners, and we decided to look forward and realize that the foundations which most of our key institutions stood upon had been occupied and lost. Instead, we read everything that Doctor Malone had written about, and even the implications in the white spaces in between what he wrote. The number one thing we saw which had been lost was integrity. We posited that to destroy and raze the institutions already occupied by greed and corruption, were going to need establish a new hill…The Hill of Integrity. We spent all weekend writing a document that declared independence from the decisions of institutions that lack integrity. We came up with ten tenants that must be met in order for us to accept the decisions of those institutions. We called it The Malone Doctrine. We presented it to Doctor Malone and his wife on October 20, 2021, and they both immediately signed the document and have incorporated this into their foundation. They envision that over time, as we dig out of the corrupt hole we find ourselves in, that institutions will adopt the Malone Doctrine as a core article of behavior and will abide by it to the utmost of their ability. Furthermore, we propose that institutions which lack integrity should not be allowed to impose their decisions on the rest of us until they adopt the principles of the Malone Doctrine.

Dr. Malone and his wife Jill asked me to be on the board of the Malone Foundation and I was honored to join. Over the next few months I informed Doctor Malone that I would be monitoring the life insurance companies and funeral home results to confirm what we had suspected which was that excess mortality and disability were being caused by the vaccine.

Data Fraud, Life Insurance, CDC Excess Mortality & US Disability

In the first week of January 2022 OneAmerica CEO Scott Davison made comments on an Indiana Chamber of Commerce meeting that were picked up by Reporter for The Center Square Margret Menge:

“We are seeing, right now, the highest death rates we have seen in the history of this business – not just at OneAmerica,” the company’s CEO Scott Davison said during an online news conference this week. “The data is consistent across every player in that business.”

Davison said the increase in deaths represents “huge, huge numbers,” and that’s it’s not elderly people who are dying, but “primarily working-age people 18 to 64” who are the employees of companies that have group life insurance plans through OneAmerica.

“And what we saw just in third quarter, we’re seeing it continue into fourth quarter, is that death rates are up 40% over what they were pre-pandemic,” he said.

“Just to give you an idea of how bad that is, a three-sigma or a one-in-200-year catastrophe would be 10% increase over pre-pandemic,” he said. “So 40% is just unheard of.”

Most of the claims for deaths being filed are not classified as COVID-19 deaths, Davison said.

He said at the same time, the company is seeing an “uptick” in disability claims, saying at first it was short-term disability claims, and now the increase is in long-term disability claims.

This stunning revelation set off flares for Doctor Malone and myself, and Doctor Malone began working to elevate my relatively small social media presence and was able to get me on Steve Bannon’s War Room. I had already done some media and had been quite loud that the clinical trial data at Pfizer was fraudulent based solely on the fact that the FDA in November said they would hide the data for 75 years, which for me was prima facie evidence of fraud and a cover up. It was then that I realized the FDA was in on the fraud and was completely captured. Eventually Moderna & Pfizer will be held accountable for this fraud.

After first appearing on Bannon’s War Room saying that the vaccine program was based on fraudulent data, I said I would be monitoring the results of Insurance companies and funeral homes for the fruits of their fraud. Unlike financial frauds the damage here was not monetary but human lives and long-term health. I also stated I wanted to be a lightning rod, and two individuals came forward to assist my effort.

The first of these was Brook Jackson, who was the Antavia Whistleblower who witnessed data corruption of the Pfizer 28-day clinical vaccine trial. She oversaw 1,000 of the 44,000 patients enrolled in the clinical trial, and the most egregious thing she witnessed was the unblinding of the patients. This was a direct violation of Pfizer’s own protocols, and the data should have been thrown out. Instead as a reward for reporting this to the FDA, Brook was fired and the data made its way into the clinical trial. The number of patients during the 28-day trial that the 95% effective rate was predicated upon was so small, that mathematically just Brook’s clinical research site could have altered the results and rendered the vaccine completely ineffective. Real world experience has proven that at a bare minimum the vaccine does not work in stopping infection or transmission. This was the original sin and genesis of the fraud. Brook’s sites were given awards by Pfizer for apparently doing such a good job. Obviously, where there is smoke there is fire, and it can be easy inferred that other sites also engaged in unblinding of the patient data. The impact of this unblinding is important to understand, as maintaining the integrity of the data blinding system is the cornerstone of the integrity of any drug trial. Because unblinding can introduce bias, and can easily lead to doctors not testing patients who present illness as having had COVID because they can look at the chart and see the patient had the vaccine and decide not to test for COVID due to a bias of assuming that the vaccine is effective. After speaking with Brook, I concluded that my suspicions of fraud were confirmed, and we did an interview together with the Thomas Paine podcast where this fraud was highlighted. Brook is currently engaged in a lawsuit with Pfizer where it has come up recently that one of Pfizer’s defenses is that its ok that they engaged in fraud because the US government was aware of it. Why this is not the largest mainstream media story is testament to the corruption of the press by government money.

The second individual to come forward to assist me in my analysis of the insurance industry was Josh Stirling. Mr. Stirling was a former #1 ranked Institutional Investor Wall Street Insurance Analyst who worked for Sanford C. Bernstein Research. He had us focus on the loss ratio of the group life and disability divisions of the life insurance companies. The reason we did that is because this is a stable business which is very profitable for insurance companies. It’s basically a typical death benefit and disability policy offered to mid-level employees when they join a corporation. The death benefit is de minimis in dollar amount, and never is expected to be collected as (statistically speaking) working age people don’t die in large numbers when they are healthy and employed with good jobs. What we found was stunning and confirmed what the One America CEO saw in January. The Q4 results from some of the major insurers saw a range of increase in their loss ratio of between 25% and 45% from 2019 base line levels, and there was a continued rise from Q3 2020 results. Many of the CEOs blamed this huge increase on COVID, and they developed and then blamed this increase on a strange new concept they termed indirect COVID. Disability also saw a marked increase and still continues to climb today. Josh and I suspected that the insurance companies which didn’t have these types of losses and excess mortality in the early part of the year was because the corporate mandates instituted by the Biden administration began in the fall of 2021 which coincided with huge uptick in the deaths and losses the insurance companies experienced in Q3 and Q4 of 2021. Remember these are working age people, and as a group were not affected by COVID in 2020 before the vaccines were deployed. However, suddenly they began experiencing a huge uptick in excess all-cause mortality. Using simple deductive reasoning, Josh and I concluded that the only thing that changed from 2020 to 2021 was the vaccination program and the mandates.

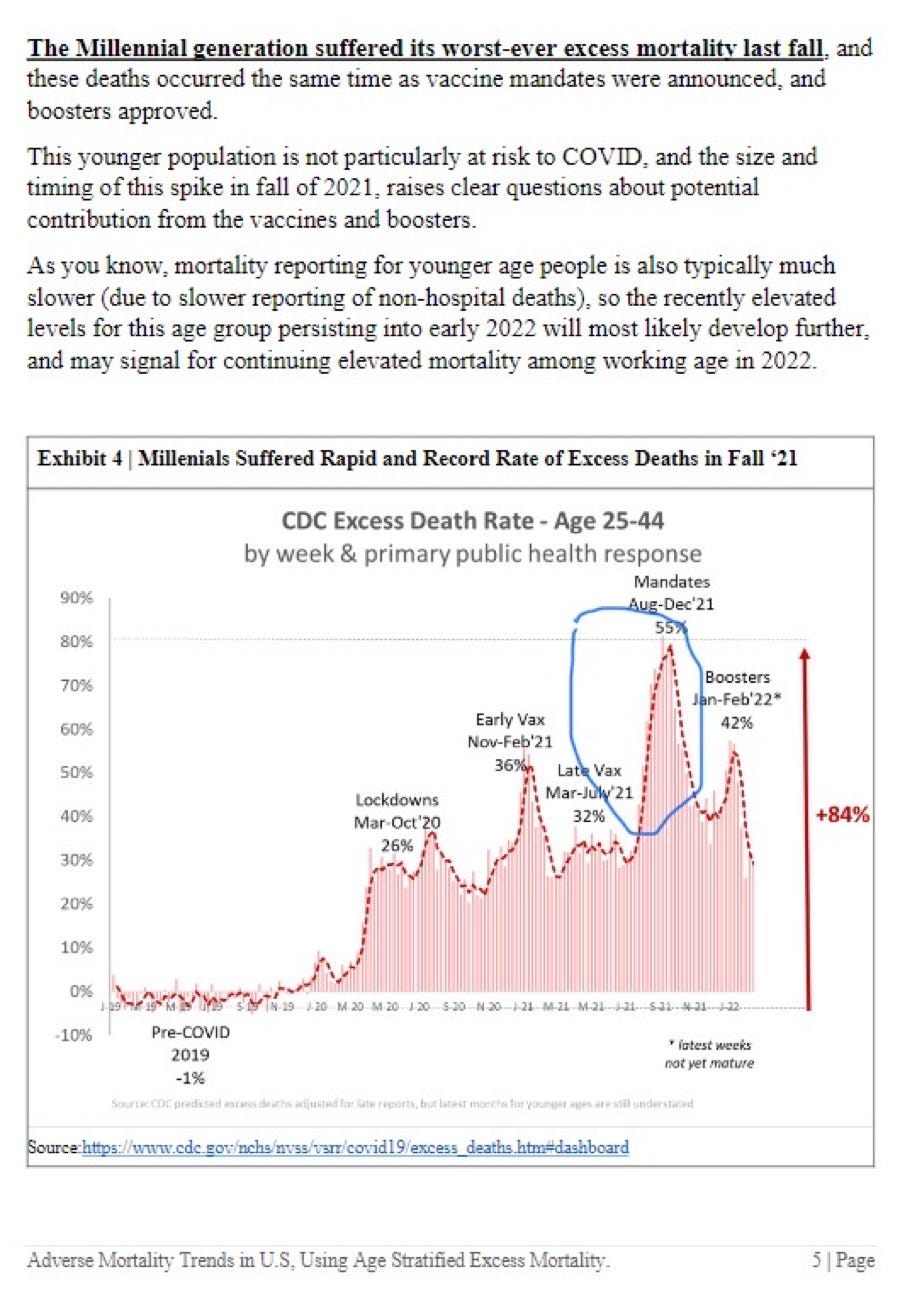

Next my partner decided to look at the CDC excess mortality data. The data as presented on the CDC website was not very helpful as they lumped all ages together. That chart in itself was damning as it showed two spikes of excess mortality. The first spike was during the fall-winter of 2020, then there was a subsequent spike into the fall of 2021 which was almost but not quite as high. That alone would suggest gross incompetence by our health officials, especially given the supposed introduction of miracle vaccines which according to them prevented infection and transmission (both of which statements have since been shown to be lies). However, Mr. Stirling was able to grab the data from the website and break it down by age. He developed baseline mortality analyses from 2015-2019 (which was pre-COVID) and then developed excess mortality charts over time for each age group. What he found was simply stunning, and both of us suddenly confronted the implications. This analysis effectively confirmed the results we saw from the life insurers in their financial reports. Millennials saw an acceleration of excess mortality into the second half of 2021 to new all-time highs, a stunning 84% above baseline. The rate of change during the fall vaccine mandates was particularly striking for us, as it coincided with the surge of corporate vaccine mandates during that time. We called this the smoking gun chart. The virus didn’t decide to affect a different age group in the fall of 2021, suicides didn’t magically all happen in a three-month period, nor overdoses or missing cancer screening in a three-month period. The only thing that changed was that genetic vaccine products were forced upon the millennial generation via government and corporate mandates. We summarized this stunning finding in a series of graphs such as the following:

The second most important discovery that Mr. Stirling found was the shift in the mixture of mortality from old to young which occurred from 2020 to 2021. In 2020 there were 592,000 excess deaths with 126,000 under the age of 65 (approximately 21%). In year 2 of the outbreak, there were 512,000 excess deaths with 181,000 under the age of 65 (approximately 35%). The millennials saw the greatest percent increase in mortality of 45% from 42,000 to 61,000 . It is hard to explain the mix shift in year 2 of the pandemic as being due to COVID, because the strains were already mutating and were becoming less virulent, and we had already determined that the virus affected mostly older people with comorbidities. It’s important to note that 45,000 more people died under the age of 65 in year 2 versus year 1. Did the virus suddenly decide to only target younger folks disproportionately? Did the virus change from respiratory to pulmonary in year 2? The only thing that changed in year 2 was the introduction of the vaccine and the subsequent mandates, which is the obvious culprit based on simple deductive reasoning. However, the authorities and the corporate media simply refuse to acknowledge much less comment on this data. The reason it is not allowed is because if the data were discussed, the obvious question would begin to be asked about the vaccines- are they really safe and effective?

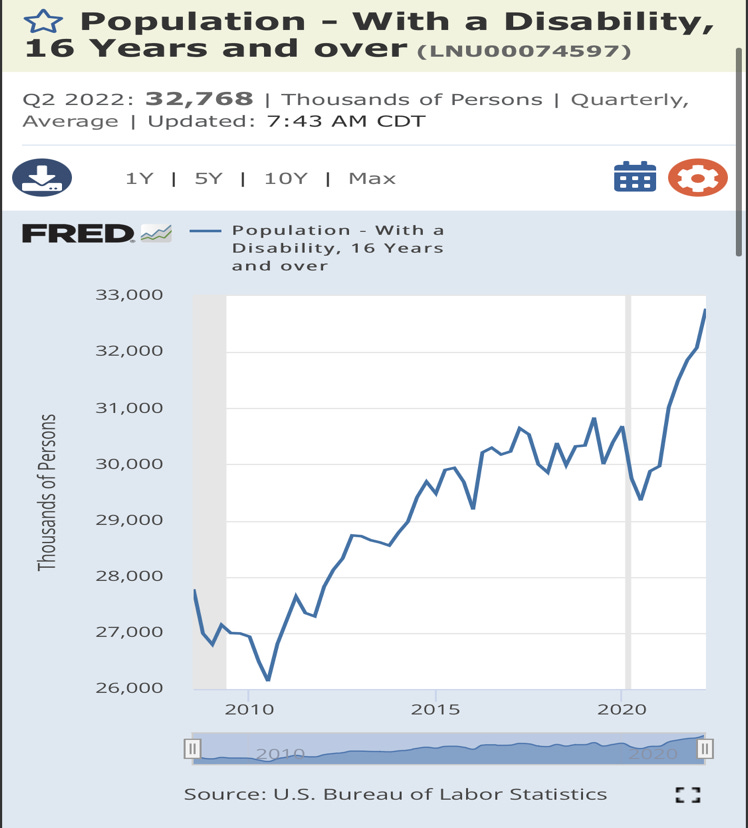

In the first week of June 2022, Mr. Stirling and I discovered another database collected by the US Bureau of Labor Statistics. This is the department responsible for the monthly household survey that delivers the employment report we see every month. The US Bureau of Labor Statistics also routinely ask a number of questions that relate to disability. This is a monthly real time survey, where the surveyed respondent answers as to whether they are themselves disabled or if there is someone in their home who identifies as disabled. This statistically derived number is not tied to claims or a doctor’s note, but rather it is based on self-identification. This is important to note, because it gives a very good real time idea of disability trends in the US. Prior to the vaccines, the run rate was about 29 million give or take for the last five years. Since the introduction of the vaccines in 2021, the number of self-identified disabled Americans has increased by 13.7% as of June 2022 from the prior run rate. This represents a numerical increase of about 4 million Americans. The graph illustrated below shows the steep rate of change that continues today. In my opinion, these data reflect an ongoing national disaster. I suspect the labor shortages we are seeing are heavily influenced by this number and can also explain much of the inflation in wages we are seeing. Again, based on deductive reasoning, the simplest explanation for this increase is that the disability is caused by the genetic vaccines. When pressed, the establishment claims that this is due to long COVID, but they most officials and corporate press outlets are ignoring and not talking about this national tragedy.

I also took a look at funeral home results, and consistent with the findings from the other databases, business has been quite good for publicly traded funeral homes with the second half 2021 number of funeral contracts accelerating into the end of the year and continuing into 2022. The commentary from funeral home executives during Q1 of 2022 from many of the companies was interesting. They were mostly surprised by their own results, and one company even said the deaths they were seeing could not all be explained by COVID. Service Corporation International hit all-time highs and has been outperforming the S&P 500 return for well over a year and a half. One would think that with the pandemic supposedly over and the introduction of “miracle” vaccines that funeral homes would be seeing business return to normal trends. That assumption however would be wrong, and (unfortunately) Funeral home stocks are growth stocks at the moment.

Final Thoughts and Implications

My stock picking career was successfully predicated on pattern recognition, making an investment thesis with limited information, taking an initial position, being early and being right over time as my thesis was either proved or disproved. Essentially, during my career I had learned to become a stock picking “conspiracy theorist”. Those that want to call me that now are welcome to do so, but I firmly believe that my thesis on the link between global debt, central banks and COVID will be borne out over time and has gained more legitimacy since my initial and “crazy predictions” during May of 2020. With regards to the vaccine data fraud, every week that rolls by seems to produce more evidence of malfeasance by Pfizer and Moderna which are unearthed by Dr Naomi Wolf’s dedicated volunteers perusing the clinical trial data dumps that the FDA wanted (unsuccessfully) to hide for 75 years. The evidence of excess death and disability continues to pile up weekly. I can say with complete certainty that I have never been more convinced in my whole career of the fact that the vaccines not only don’t work, but that these are the deadliest vaccines ever introduced into the human population on such a global scale. The US government is guilty of democide with their forced mandates, and countless corporations and government agencies are also likely liable for forcing employees to accept injections of experimental vaccines which employ novel gene therapy-based technology. The corporate media and large tech companies are also complicit due to their censorship of the nature of these vaccines, and in my opinion are accessories to wrongful death. The single greatest implication is that once we succeed in opening up the Overton window of allowed discourse on this topic, and the majority of the population gains the knowledge of what has happened, we will witness an incredible loss of trust in our institutions. At a bare minimum the NIH, CDC, FDA and Health and Human Services need to be razed and built up again anew. In addition, the politicians involved, the unwitting Doctors who pushed this vaccine program, University Administrators-departments and the media-tech complex have all lost the trust of the public, will need to rethink their institutions and governance structures, will have much to answer for in the coming years.

0 Comments