A trader in the Wheat Options pit at the CME Group throws up his arms as traders toss confetti at the closing bell for the year on December 31, 2009 in Chicago. UPI/Brian Kersey/Alamy

Food inflation: The math doesn’t add up without factoring in corporate power

by GRAIN | Mar 21, 2024

Large farmers’ protests broke out in at least 65 countries over the past year. From India to Kenya through Colombia and France, desperation has hit a breaking point. Farmers warn that without better prices and more protection, their future is at risk. Peasant movements like La Via Campesina, for over three decades now, have denounced the World Trade Organisation and the growing number of bilateral free trade agreements for destroying their livelihoods.

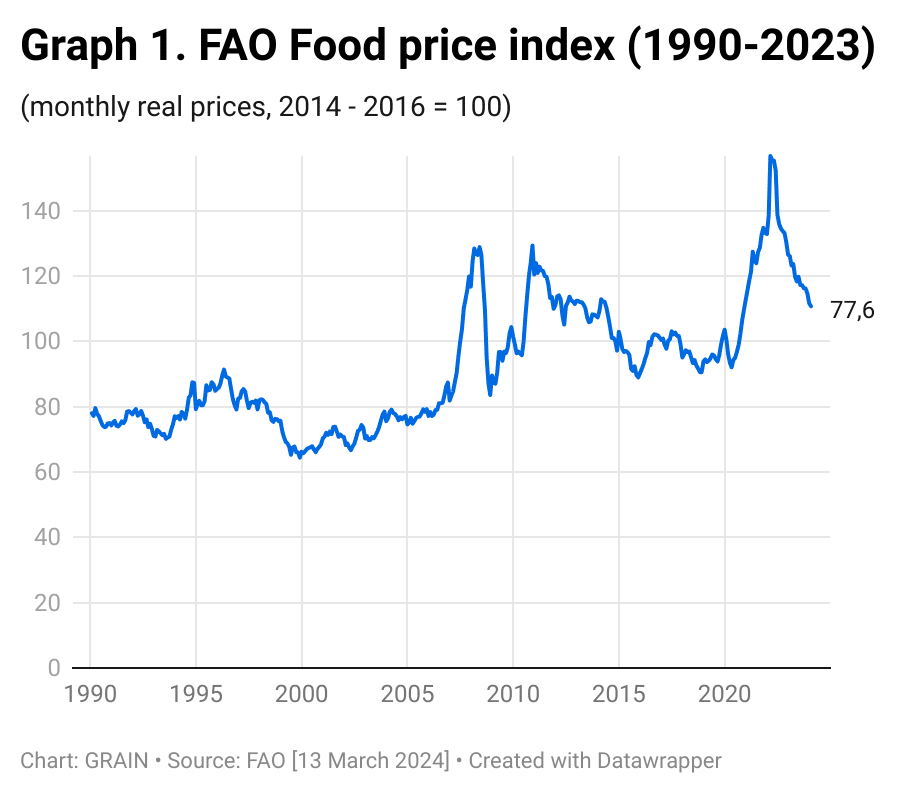

However, these protests unfold against the backdrop of record-high global food prices. The prices spiked first during the pandemic and then again at the start of the war in Ukraine hitting an all-time high in 2022. Food prices have been rising faster than other products: if the global general consumer price index (CPI) doubled between 2021 and 2022, the food CPI inflation almost tripled. According to the World Food Organisation (FAO) food price index, even if international prices have moderated in 2023, they are still higher than in 2019 (see Graph 1). And all indications are that this is a crisis of prices, and not a food shortage at the global level. For the past 20 years, world grain production has exceeded available stocks.

The impact of these food price increases on millions of people, especially the poor, is devastating. In 2022, 9.2% of the world’s population was chronically hungry, an increase of 122 million people since 2019.

But, as this year’s farmers’ protests make clear, the increase in food prices is not going into their pockets. So, who is benefiting from these food price rises?

Volatility by design

The FAO and corporate executives have attributed recent food price increases to disruptive supply chains for oil, gas, fertilisers and staple goods. This is a half truth, and thus deceptive. They don’t mention how the current structure of the food system encourages and amplifies such disruptions.

For decades, the World Bank and the International Monetary Fund (IMF) have promoted structural adjustment policies, and green revolution technologies (hybrid seeds + chemical pesticides and fertilisers) across the world. We now have a global food system designed around the production of a small number of agricultural commodities (wheat, rice, maize, soybeans, palm oil) in a few areas of the world totally devoted to the massive industrial production of monocultures dependent on the supply of inputs, and concentrated in the hands of a few companies. Any disruptions within this global system, be it war or drought, can have major impacts on people’s access to food. This is particularly acute in countries of the global South that are now highly dependent on food imports because of policies imposed on them through multilateral banks and free trade agreements. Moreover, we are entering a period of intense climate crisis, water crisis, geopolitical tensions, and declining crop yield gains that are set to generate more frequent and more severe disruptions.

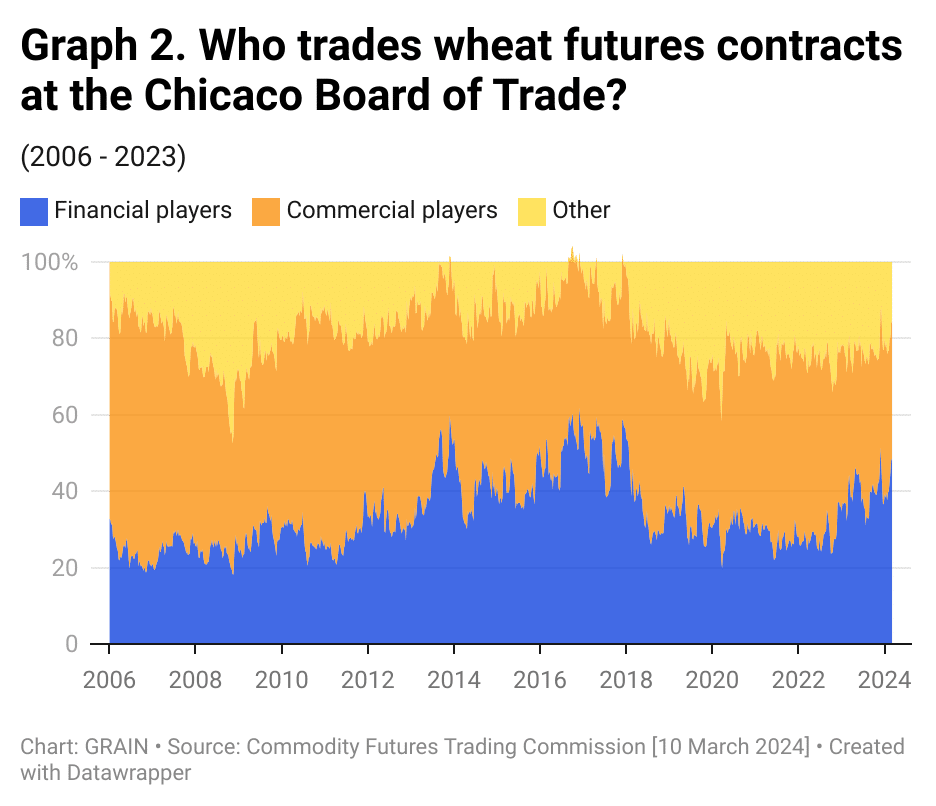

For some, however, this volatility is an opportunity. Because of deliberate policies implemented since the 1980s (see box), there is today a large and growing part of the financial sector that profits from shifts in food prices using what are called “derivatives”. In theory, the use of these instruments helps buyers and sellers to lock in prices and protect themselves against the risk of price fluctuations. The most common and important of these instruments are futures contracts, which are agreements to buy or sell agricultural commodities at a specified future date. In futures markets, it is not the agricultural product itself that is traded, but the contract. The price of the contract changes according to supply and demand. But price variations on the futures markets have a direct influence on price fluctuation of the goods to which the futures contract relate. For example, if the price of a wheat futures contract rises, this indicates that the estimated future price of wheat is high. Consequently, the real current price of wheat rises. With increased activity in the financial futures markets, food trading has come to be referenced to futures prices. In a vicious circle, the volatility of food prices attracts more speculative money into the commodity futures market. This, in turn, amplifies the volatility of the futures markets and pushes up or down real food prices.

The price volatility experienced during the 2007 – 2008 food price crisis was partly a result of a surge in financial speculation. Similarly, when the war in Ukraine began, investments in commodity futures and commodity-linked funds rocketed. Speculative positions in the Paris wheat market increased from 35 million euros in January 2021 to 1 billion euros in March 2022. A report by IPES-Food found that the price of wheat on futures markets rose 54% in nine days, and the US Commodity Futures Trading Commission noted that volatility was 20% higher than normal. While this drove price increases that penalised consumers, hedge funds and pension funds speculating on food markets made huge profits.

The world’s agricultural trading companies have also benefited massively from this situation, including through their participation in financial markets. In 2022, profits achieved by the top five firms in this sector doubled and even tripled compared to the period 2016 – 2020. A report by the United Nations Conference on Trade and Development found that corporate profits of global food traders “appear to be strongly linked to periods of excessive speculation in commodity markets and to the growth of shadow banking – an unregulated financial sector that operates outside traditional banking institutions”.

They have some important advantages over purely financial players. For one, as ‘commercial actors’ they are not subject to the same restrictions or regulations of financial actors on commodity trading markets. Also, because of their global presence they have the most in-depth and up-to-date information about the availability of products and are the first to know about poor harvests or bumper crops. A study by SOMO found that the largest agricultural commodity trading companies ADM, Bunge, Cargill, COFCO International and Louis Dreyfus (usually referred to as “ABCCD”) control 73% of the global grain and oilseed trade as well as a combined 1 million hectares of farmland.

A perverse and well prepared alignment of the stars in the 1980s

Three parallel developments in the 1980s were key to financialising the global food system. First, the liberalisation of agricultural markets was promoted by the World Bank and other international agencies. Until then, governments in different regions had adopted policies to protect farmers from production risks. Second, financial markets were deregulated in the United States and investment banks and commodity trading firms began marketing index funds that tracked the prices of various commodities. In addition, large institutional investors (such as pension funds) sought to diversify their investments. To hedge their risks, they increased their investments in commodity derivatives and physical assets. As a result, a growing number of financial players began to speculate on food prices. Third, like other companies, agribusiness companies experienced a dramatic shift in ownership with the entry of large asset management firms. CEO salaries became linked to the value of shares, creating a strong incentive to restructure companies in ways that generated more profit for shareholders. To this end, mergers and acquisitions multiplied, laying the foundations for today’s deep corporate concentration in the agri-food sector.

Source: Jennifer Clapp and S. Ryan Isakson, “Speculative Harvests: Financialization, Food, and Agriculture”, Agrarian Change & Peasant Studies, 2021.

Price manipulation and sellers’ inflation

Financial markets are not the only space where big agribusiness and food companies have an impact on food prices. A growing number of voices, such as the economist Isabella Weber, point to the monopoly power of corporations as a major factor in recent price inflation, including with food. What they call “sellers’ inflation” happens in contexts of supply-chain bottlenecks and cost shocks. When price hikes in upstream sectors (such as the gas needed for fertilisers) spread along the supply chain, companies in downstream sectors pass on cost increases to protect margins and even take the opportunity to increase margins. They can raise prices knowing that all their competitors will do the same.

Such strategies are only possible in contexts where a handful of companies have the power to set prices, as is the case in the food and agriculture sector. For example, just four companies, Bayer, Corteva, Syngenta and BASF control half of the seed market and 75% of the global agrochemicals market. Since 2018, their profits have nearly doubled. On the fertilisers side, the global market is controlled by a small number of companies. Four of them control a third of all nitrogen fertiliser production. From 2018 to 2022, the profits of the top 9 fertiliser corporations more than tripled, as they increased prices far beyond the production costs. Another example can be found in the world’s second largest meat processor, Tyson. The company more than doubled its margins and profits at the end of 2021. This was due to price increases it initiated and then continued to raise to protect margins against cost pressures from grain prices. A similar strategy was followed by large branders as Nestlé, Unilever and Mondelez who increased prices and ended by recording high profits in 2022.

This combination of monopoly power and unregulated activity in financial markets allows agricultural commodity traders, big agribusiness and food companies to make huge profits from food price rises.

Countering corporate power in food systems

The big culprit when it comes to today’s high food prices for consumers and low prices for farmers is corporate power. The climate crisis will only make this situation worse, unless urgent actions are taken to dismantle corporate power and shift to more localised food systems, based on diversified food production and catered to people’s food needs. The struggle against free trade agreements, at the forefront of many of today’s farmers’ protests, is therefore critical.

At the same time, actions are needed to reign in the power of those actors in the casino economy who are amplifying food price volatility and increases. When it comes to financial speculation, an important driver in food price volatility, regulations need to be tightened. And, to tackle the so-called “sellers’ inflation”, we need measures to prevent profiteering, which could include taxes on windfall profits anti-trust measures, and, more importantly public controls over food prices and programmes that ensure a fair, equitable and secure distribution of nutritious foods to everyone.

Subscribe to GRAIN

0 Comments