The dominant trend of US social life over the last fifteen years is a stagnating, and then declining, life span. There are many reasons for this trend, such as violence, diet, suicide, drug addiction, and auto accidents. But for many reasons, our monopolistic health care system is a big part of the problem.Monopolistic drug wholesalers fostered the opioid crisis, and now, for the same reason, they are creating shortages of prescription drugs. Untreated mental illness is a significant factor in elevated suicide rates. Not being able to get care when you need it is associated with higher levels of death and permanent injury. More fundamentally, knowing that there are no systems in place to protect or care for you undermines any sense of hope.

It’s easy to describe what is happening as consistent with an overall pessimistic tale about the U.S., one that is almost uniquely American. The story goes that in the U.S., the richest country in the world, citizens can’t get access to a doctor when they need it. Most of Europe, and most countries globally, have universal health care, and some have had it for more than a century. By contrast, we’ve never had it here.

America almost achieved universal health care multiple times. Teddy Roosevelt proposed it, so did Harry Truman, Richard Nixon, Jimmy Carter, and Bill Clinton. They failed, largely because of the powerful doctor lobby — the American Medical Association — standing against it.

But if you look at the story from the perspective of most Americans instead of the system at large, the story is not so rigid. For much of the 20th century, the American health care system was one of very high quality, with great doctors, hospitals, and an exceptionally innovative, if overpriced, pharmaceutical system.

And access generally did increase, quite dramatically. We organized our health care system by letting people collectively get together, pool their money, and use this pool to pay for medical care when any member needed it. From 1950 to 1965, the percentage of Americans with surgical coverage jumped from 36 percent to 72 percent. In the 1960s, as historian Alan Derickson noted, “health insecurity became the exception rather than the rule.”These pools are known as insurance companies, and today they represent the classic dilemma of using ‘other people’s money’ that Brandeis noted in the early 20th century. Even so, health insurance is very good to have. And in 2010, the uninsured population in the U.S. was 45 million, or 15 percent of the country. That’s too many.

While there has also been frustration that insurers don’t cover what they should, trying to penny pinch, and costing lives in the process, for most Americans, the assumption was that the care is pretty good. And it often was. So access, not quality, is the fulcrum for political debate, along with some critiques of health insurers who refused to fully cover necessary services.

Yet over the last twenty years, something fundamental in the American health care system has changed. It’s not that people can’t get insurance; indeed, America is more insured than it has ever been. It’s that the underlying quality inside the health system is falling apart. One obvious signpost, of course, is that doctors, distributors, and pharmaceutical companies helped hook Americans on heroin-style substances from the late 1990s onward, leading to the deaths of hundreds of thousands of people. But it’s more than that scandal, as gruesome as it is.

Americans spend more on care, and get less, than any other country. And the reason for the dysfunctional care is that since the passage of Obamacare, the firms who control our health care system have become far bigger, and much more powerful.

The hospital sector, for instance, represents a third of health care spending. Starting in the 1980s and accelerating after Obamacare, hospital systems have merged into giant monopolies, driving huge price hikes and increasingly poor quality. Private equity has come into everything from ambulances to urgent care to nursing homes. Monopolistic Group Purchasing Organizations have created shortages among hundreds of drugs, which reduce the equality of care. These are known problems, and real.

But the one area where we’ve seen the emergence of a different and fundamentally corrupt business model is the insurer space. In 2007, for instance, UnitedHealth Group, one of the country’s biggest insurers, had total revenues of $75 billion. In 2022, the firm, having expanded far beyond insurance, had annual revenue of $325 billion. CVS Health, which bought insurance giant Aetna in 2018, had a similar trajectory, with $76 billion of revenue in 2007, and $322 billion in 2022.

UnitedHealthcare is not just an insurer, it employs around 50,000 physicians, it sells software. CVS is the largest pharmacy chain in the country and has a network of clinics, while Humana is now the biggest provider of home health care services in the country. Insurers control home health agencies, ambulance providers, and data management firms, as well as pharmaceutical middlemen.

Consider a few recent stories about how these firms operate. Last year, ProPublica and The Capitol Forum did two investigations into the health insurance industry. In one story, their reporters profiled a UnitedHealthcare customer named Christopher McNaughton who suffers from a crippling case of ulcerative colitis and requires expensive medicine. UnitedHealthcare didn’t want to pay, so it rejected claims paying for McNaughton’s care, deeming it “not medically necessary” and lying about what his own doctor said. McNaughton’s doctor fought for him, he sued, and he was able to keep paying for medicine and stay alive. But it was horrific.

In another, separate story, reporters found that Cigna, encouraged by private equity, engineered its system so that customers who filed claims for care would be automatically rejected. This practice, of denying care to those who paid for it, is likely industry wide.

One might ask why customers would buy insurance from firms who automatically deny claims. Once again, it’s a monopoly issue. Today, three quarters of markets are highly concentrated, and almost half have one insurer with more than 50 percent of the market. Most people can’t choose their insurer, their employer chooses for them. And it’s compelling to buy from a big insurer, because it’s more likely a local doctor and hospital are in their local network, at better rates. McNaughton, after years of lawsuits, still buys his insurance from UnitedHealthcare.

Other People’s Money

What is weird about the American health care fiasco exposed by ProPublica and The Capitol Forum is that we had supposedly addressed it.

Fourteen years ago, America had a bitter debate over health care access, and President Barack Obama won his fight for what was ostensibly universal care. There were also supposedly rules about denying people coverage. In 2010, the United States Congress passed the Affordable Care Act (ACA), and President Obama signed it into law. This law was largely targeted at the payers in the system — insurers — and not so much providers — the entities who deliver care, such as hospitals, doctors, clinics, pharmaceutical companies, ambulances, etc.

The passage of this law was fraught. Obama didn’t want to let private health insurers sabotage his health care crusade the way they had Bill Clinton’s attempts in the early 1990s, the so-called ‘HillaryCare.’ The strategy Obama chose was to co-opt insurers with sticks and carrots.

The stick was that if they didn’t get on board, they’d be punished with a genuine national system that might push them out of the market. The carrots were more extensive. The law forced millions of people to become customers of these private insurers. It also expanded the health insurance program for the poor, known as Medicaid, which could be profitable for private insurers. Finally, Obama didn’t stop private insurers from privatizing Medicare, which remains enormously profitable for them. So the insurers got on board.

Despite these concessions, health policy wonks generally liked what Obama had done, because it took on the main problem which was, as they saw it, access. Obamacare was designed to expand health insurance coverage to most people who didn’t have it, and in that sense, it delivered. The number of uninsured Americans dropped from 45 million to 27 million within just a few years.

And yet, something was off. Obama had promised on the campaign trail that he would sign a universal health care bill into law, and one that would “cut the cost of a typical family’s premium by up to $2,500 a year.” In 2004, the average insured family of four paid $11,192 in health care costs; by 2022 that amount was $30,260. That increase in cost for a family of four is the price of a small car, every single year.

And that’s because prices have gone up, and not because there are more doctors, beds, or care. While Obamacare did expand access, it didn’t address the key problem in the U.S. health care system: monopoly power. So prices kept rising. And still are.

To understand how it went so wrong, it helps to look at the one key place where policymakers tried to impose real cost controls on insurers, and how that attempt backfired.

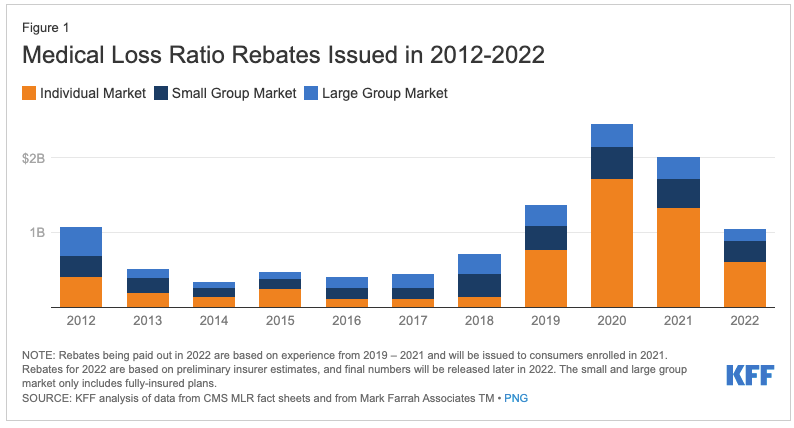

The provision of the law most hated by payers during the Obamacare fight was known as the Medical Loss Ratio, a provision authored by then-Senator Al Franken, which required insurers to spend a certain minimum percentage of the premiums they collect on medical care compared to administrative costs (including executive salaries). For some plans, the minimum was 80 percent, for others it was 85 percent. If insurers spent below that amount, they would have to mail the difference out as a rebate to customers.

The Medical Loss ratio was essentially a public utility rate regulation capping profits for private health insurers. And it made a lot of sense, intuitively. Payers could make some money, but they would have to spend on care. If they didn’t spend what they collected, they had to return extra money, which means they had an incentive to lower prices.

At first, this provision seemed to work. The health care nonprofit KFF reported that consumers saved an average of 7.5 percent on their health insurance within the first few years, as payers mailed out hundreds of millions of dollars every year to customers.

After the passage of the Affordable Care Act in 2010, health insurance companies pursued a variety of strategies to increase profits. They focused on different kinds of products, especially Medicare Advantage plans targeted at older Americans. And they sought to buy up rivals, hoping to bulk up.

Aetna tried to buy Cigna, and Anthem sought to combine with Humana. These were so-called horizontal mergers, which is to say, firms seeking to combine with rivals who sold the same products they did. Their goal was to simply grow their way out of the problem. If you can only make a 15 or 20 percent margin, well, at least you can still increase your revenue. In both cases, however, the Obama antitrust division sued, and won.

So insurance company executives figured out another strategy. Why not become more than a health insurance business? After all, if you’re both a payer and a provider, you can tap into that other 85 percent by directing insurance money to providers you control.

And so a new kind of merger trend in health care accelerated. Not horizontal acquisitions, but what are called vertical mergers. Health insurance giants stopped trying to buy each other, and started to buy or be bought by entities with whom they negotiate to buy services. It was “payers” buying or being bought by “providers.”

Before the Medical Loss Ratio, “payers,” which is to say insurers whose job was to buy billions of dollars of goods and services for their customers, sort of had an incentive to hold costs down. They usually did this by being jerks to customers, denying them care they needed.

But once the government capped insurer profits at 15 percent of insurance revenue, these firms had a different incentive. They sought higher revenue and higher spending, instead of cost controls. They also wanted to buy providers so they could get access to that other 85 percent of the revenue. What better way to make money than by being both the buyer and the seller?

Richard G. Frank and Conrad Milhaupt from Brookings noted this trend last year. Payers could buy providers, and then send revenue to related businesses. The two firms leading the charge were UnitedHealth Group and CVS. UnitedHealth, one of the big four insurers, formed a subsidiary in 2011 right after the passage of Obamacare called Optum. Optum began rolling up physician’s practices, software and analytics firms, medical clinics, and pharmaceutical middlemen.

In 2018, CVS, which owned large pharmacy chains and the pharmacy benefit manager Caremark, bought the health insurer Aetna. Earlier this year, CVS completed its acquisition of Signify Health and Oak Street. In 2018, Cigna bought Express Scripts, the largest pharmacy benefit manager in the country. Humana bought Kindred, a health care delivery firm. Elevance, formerly Anthem, became a pharmacy benefit manager, and cut deals with a large number of medical providers.

In 2019, UnitedHealth sent 18 percent of its payer revenue to itself, while CVS’s Aetna sent 13 percent to its own clinics and pharmacies. That number has no doubt increased dramatically over the last three years.

The Need For A Glass-Steagall In Health Care

There have been hundreds of acquisitions since the Affordable Care Act was signed, and the American health care system is now a whole different beast. Talking about insurers, or pharmacy benefit managers, or drug store chains, or doctor practices in isolation, simply doesn’t make sense anymore.

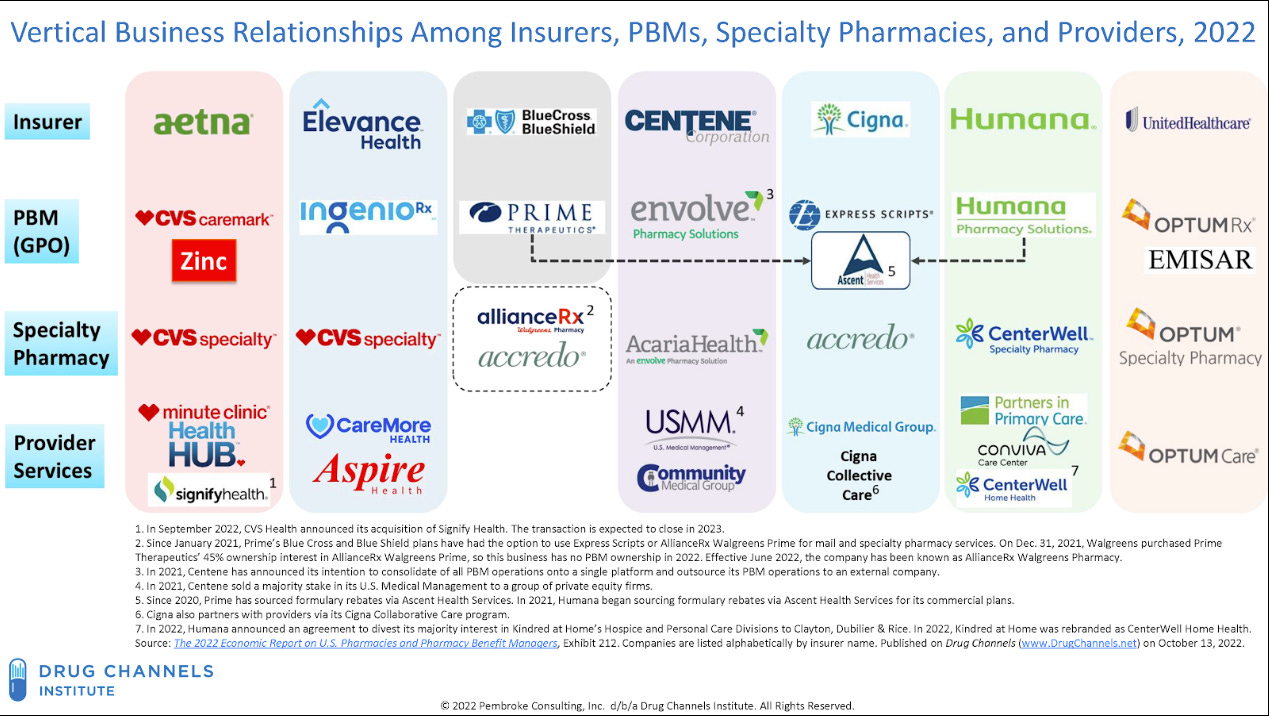

We are dominated by health care conglomerates. A few years ago, the Drug Channels Institute showed this dynamic with an infamous chart, purely in the drug middleman space, mapping out immense and confusing consolidation.

The shift in the practice of American medicine has been fundamental. You simply cannot hang a shingle and become an independent doctor or pharmacist, because it is impossible to get reimbursed in any reasonable manner. Becoming a doctor today means you are going to be an employee of a giant conglomerate or hospital chain.

And the prices for consumers, whether through premiums, deductibles, co-insurance, or any of the other sadistic methods dreamed up by health care actuaries, are higher and more confusing. Health care benefits increasingly include consulting services to help navigate health care benefits, which is insane. And that’s if you’re well off.

The heart of the problem is that there is a conflict of interest between being a payer and being a provider. If I’m choosing to spend money on behalf of a customer, and I’m also on the other side of the transaction, I have an incentive to steer that purchase to where I benefit, and not solely for the benefit of the customer.

To address these kinds of conflicts, in previous eras in history, we’ve regulated industries to prohibit certain forms of vertical integration. (30 Rock’s clip on vertical integration explains conceptually what these kinds of mergers do.)

In the 1990s, for instance, when pharmaceutical firms owned pharmaceutical middlemen, the FTC forced them to divest their pharmacy benefit managers to make sure they would have no incentive to promote certain drugs over others. There are also a host of laws, like anti-price steering provisions, anti-kickback laws, and laws like the Robinson-Patman Act, that block conflicts of interest across a variety of industries. The Glass-Steagall regime was one such law in banking that kept investment and commercial banking apart — but there have been many others.

Over time, economists and policymakers came to think of vertical mergers as harmless, or even efficiency-enhancing. So when the Affordable Care Act passed, Congress didn’t do much to prohibit conflicts of interest, as the goal was access to a system that most wonks thought was pretty good. Instead, Congress capped insurer profits through the Medical Loss Ratio.

But without prohibiting the combo of providers and payers, this well-meaning public utility profit cap, combined with new demand for insurance, instead fostered a dramatic roll-up of power. Today, CVS and UnitedHealth Group are health care tyrants, and everyone else must keep pace, either through mergers or other aggressive merger-like contracting practices.

So what are the costs of this vertically integrated hell-space? The underlying quality of care is declining as health care conglomerates focus on exploiting conflicts of interest. Consider three legal actions in recent years.

In March 2022, CVS Health was sued under the False Claims Act for fraud. A whistleblower alleges that CVS was lying to its insurance customers, forcing them to buy more expensive brand name drugs when cheaper generic drugs were available. The reason CVS would lie to customers is that it would get payments on the back-end from pharmaceutical producers whose products it had helped sell. Many customers couldn’t afford those higher prices, even though the government had paid for CVS to give them a Medicare drug plan that covered the costs.

Similarly, last March, Ohio Attorney General David Yost sued Cigna’s Express Scripts subsidiary, as well as Humana Pharmacy Solutions, calling these firms “modern gangsters” for raising prices on people who needed medicine, and cutting revenue to independent pharmacists.

Yost wasn’t the only aggressive regulator. Oklahoma Insurance Commissioner Glen Mulready threatened to strip CVS of its right to operate in the state as a pharmaceutical middleman because the firm forced patients to use its poor quality mail-order and retail pharmacies instead of their preferred pharmacies, and then lied about it.

All three of these actions came about because the entity was a payer, aka it was buying things for a client, as well as a provider, which is to say, it was selling stuff to that client. And it’s getting worse, because the judiciary doesn’t recognize the threat of such vertical mergers.

CVS’ Purchase Of Signify

Another cost is low-level forms of fraud and monopolization, especially where we spend the most on health care: the elderly. Since the early 2000s, the U.S. has been privatizing the Medicare system. Most people above 65 now have their health insurance paid for by the government, but choose from among multiple private plans, in what is known as the Medicare Advantage program.

The Medicare Advantage market has rapidly become one of the largest sources of spending for the federal government, accounting for $361 billion of federal spending in 2021, and is expected to grow to an astounding $943 billion by 2031 as the population ages. Along with this growth is waste. Taxpayers overpaid Medicare Advantage health insurers by as much as $25 billion in 2020 alone, meaning nearly 8 percent of all spending in the program could have been overpayment.

The largest health insurance companies, unsurprisingly, have been capturing the market to monopolize profits. The Top 4 plan providers control around 62 percent of Medicare Advantage plans, with even greater concentration at local levels.

And it’s getting worse, precisely because of the lack of a separation between payers and providers. Last year, CVS Health acquired one of the critical cogs in the Medicare overpayment scheme — the dominant “in-home evaluation” company Signify Health — in an $8 billion deal. This acquisition is a classic payer-provider conflict of interest.

Signify Health is the number-one provider of in-home health evaluations for Medicare Advantage patients. Signify has a network of over 10,000 traveling nurse practitioners and physicians across the country who drive to Medicare Advantage patients’ houses to perform in-home evaluations that generally last around an hour, supposedly trying to help with preventative care.

Signify charges Medicare Advantage plans around $330 per patient visit. Why are the plans willing to pay $330 per visit for a one-hour service that may not actually lead to improved care or lower costs through preventative care? The answer lies in the way Medicare Advantage plans are paid. Since Medicare Advantage pays out a fixed amount per patient, and patients can have vastly different expected costs depending on their preexisting conditions, Medicare developed a system to compensate Medicare Advantage plans for taking on riskier patients.

The health status of a patient is called a risk score, which is calculated using a formula that considers all diagnosis and existing conditions of a patient. For example, if a patient has diabetes, all else equal, that patient will have a higher risk score than a patient without diabetes, and the government will pay the Medicare Advantage plan more per month for insuring that patient.

This intuitively makes sense, but in practice can lead to abuses of the system where plans attempt to make their patient populations appear less healthy than they actually are. As it turns out, Signify’s annual visits are an excellent opportunity to “diagnose” patients, and there have been accusations that Signify pushes their doctors to aggressively diagnose conditions so that plans can be paid for patient conditions that they have no intention of proactively treating.

This is not simply idle speculation. In October 2022, the DOJ sued CIGNA , alleging these practices are fraudulent. The DOJ’s complaint alleges “diagnoses codes were based solely on forms completed by vendors retained and paid by CIGNA to conduct in-home assessments of plan members.”

This brings us to CVS’s acquisition of Signify. Although Signify has already faced allegations of pushing hard to diagnose patients with conditions that would drive up risk scores, it is inevitable that it would have even more incentives to drive up risk scores under the ownership of CVS.

Currently, Signify can be motivated to push higher risk scores to please its customers (insurance companies getting paid by the federal government). However, Signify as an independent company at least has a layer of separation from the profits received by these customers from increasing risk scores.

Once Signify is owned by CVS, a risk score that increases payments from the Center for Medicare and Medicaid Services to CVS’s insurer subsidiary Aetna will directly benefit the corporate entity. CVS management will know this and be incentivized to push Signify’s clinicians to diagnose more aggressively, driving increased revenue and costing the federal government and taxpayers.

Signify is the largest in-home evaluation provider in the country, with its only significant competition coming from its much smaller competitor Matrix Medical Network. Signify’s largest customers besides Aetna (CVS) are Humana and UnitedHealth. These massive vertically integrated health care companies are likely to have the bargaining power to remain important customers of Signify. After all, Signify will need additional volume besides just Aetna customers to profitably maintain its 10,000 clinician network.

The real victims will be smaller Medicare Advantage plans that threaten to bring competition to the Medicare Advantage market. Currently, Signify is incentivized to work with all health plans in order to maximize in-home health evaluation volume and revenue. After the deal, CVS will have the ability to monitor upstart Medicare Advantage plans and either explicitly refuse to service plans that threaten to take market share or provide a degraded or more expensive product to slow their growth.

But the problems don’t stop there. CVS can spy on rivals with the data it is collecting through Signature. The incentives are obvious — CVS will have all of the data collected from Signify’s in-home evaluations, meaning it will know which patients are likely to be the most profitable as Medicare Advantage customers.

Remember, CVS will have data around each patient’s conditions and diagnoses contributing to risk scores, and have its own data around the expected profitability of patients with specific risk scores and profiles. This could lead to Aetna targeting specific patients of its competitors, making it even more difficult for small Medicare Advantage plans to compete.

Aetna could also use Signify data in areas where it does not currently offer Medicare Advantage plans to decide whether to enter that area to offer plans. This would lead to areas with less expected profitability missing out on competition from Aetna that it would otherwise have received.

More broadly, this acquisition adds another stream of highly sensitive data into the health care conglomerate CVS. CVS already controls the largest pharmacy benefit manager in the country, the largest chain of pharmacies in the country, one of the largest health insurance providers in the country, and a growing chain of primary care providers through its Minute Clinic Brand. The pharmacy down the road will now be collecting health data from millions of in-home evaluations across the country.

So What Now?

Why didn’t the Antitrust Division challenge this acquisition? Well in 2022, the Antitrust Division tried to do something about vertical consolidation, suing to block UnitedHealth Group’s purchase of Change Health, which is a dominant payment network within the health care system. But Judge Carl Nichols ruled against the DOJ, partly on the grounds that vertical mergers are usually not harmful. UnitedHealth wouldn’t want to jeopardize its reputation by taking advantage of customers by spying on them, the judge claimed.

So it’s possible that when analyzing the Signify merger or other similar acquisitions, the Antitrust Division is leery of a vertical merger challenge, for fear of losing again and wasting resources.

Or perhaps there is a bigger game afoot. Let’s return to the initial story, the denial of care by UnitedHealth of a customer with ulcerative colitis. Antitrust enforcers have realized that these episodes show a dangerous conflict of interest in the health conglomerate business model.

“What are the chances,” asked The Capitol Forum, “that a doctor who may have disagreed with UnitedHealth in the past would continue to do so if he or she works for UnitedHealth, a large employer of physicians and other health care providers?” Perhaps a broader monopolization claim, a case like that against Google for its conflicts of interest in the adtech ecosystem, is in the works.

But we don’t have to rely on antitrust enforcers. There’s also a broader political backlash brewing. Anger over Obamacare has dissipated, and politicians are beginning to cooperate to learn about and address middlemen in health care.

A contact in the space told me that when he watches hearings, he can see that Senators are much better versed in how pharmacy benefit managers work today than they were even a year before. House Republicans are leading a serious and credible investigation into pharmaceutical middlemen. Oklahoma and Ohio are Republican states, and they are the most aggressive regulators in the country, with Indiana leading on hospital costs. The Federal Trade Commission is investigating pharmacy benefit managers.

So there’s reason for hope.

Still, looking at American health care is an exercise in despair, with health conglomerates engaged in killing people for profit, with endless 10-15 percent increases in annual premiums, and with judges and policymakers not even knowing where to start. But we’ve now moved beyond the progressive frame of thinking the problem is merely access to insurance, and have come to realize that the underlying ability to deliver care is falling apart.

It’s only a matter of time before we start to reimpose some sort of structural prohibitions on the industry. It’s too ugly a system, and there are too many people dying not to try.

This story was originally printed on Matt Stoller’s newsletterBIG, where he explores the politics of monopoly power.

0 Comments